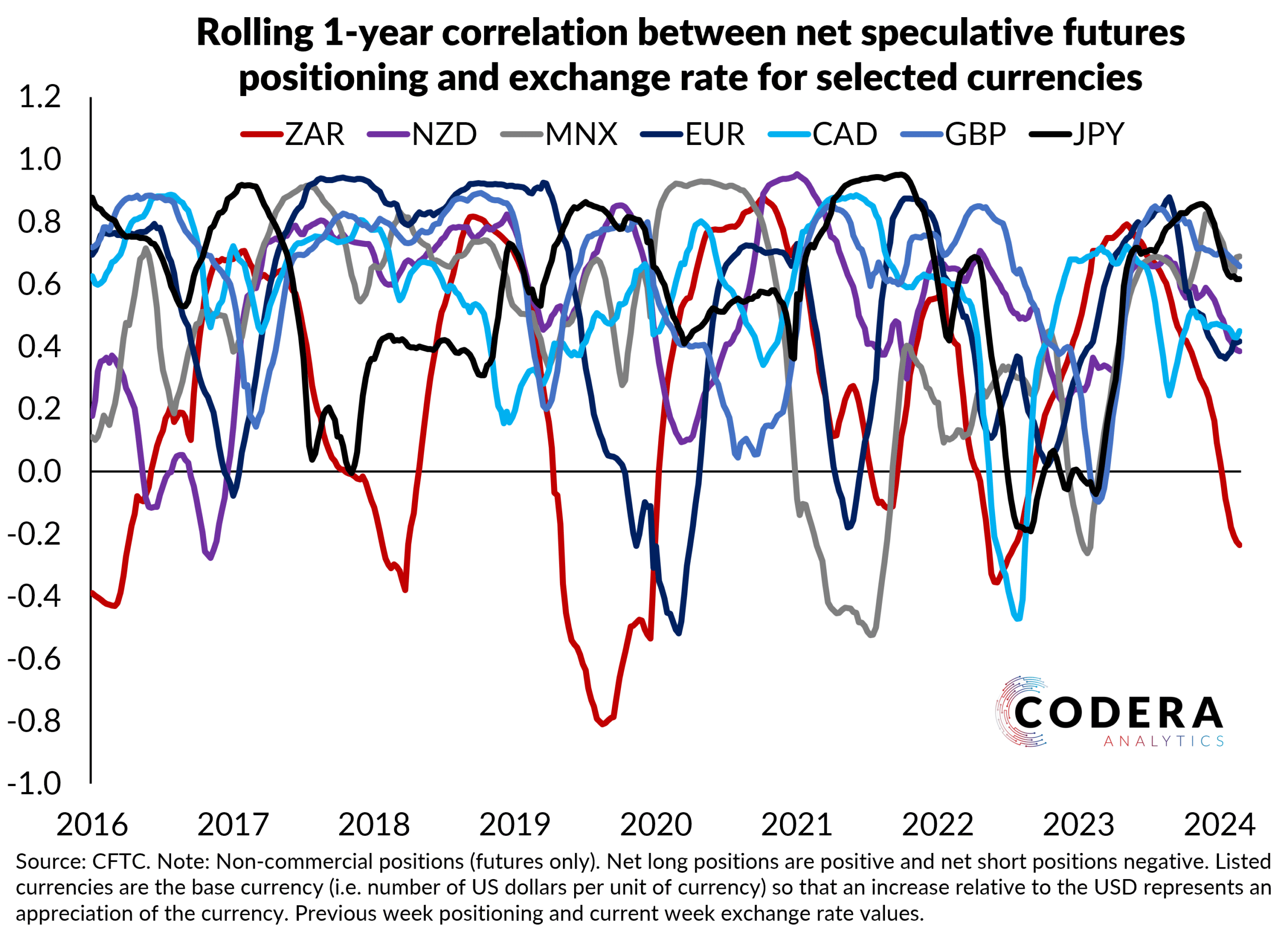

Many financial market analysts use FX positioning data to make statements about likely future movements in exchange rates. Today’s post looks at the correlation between FX speculative positioning and exchange rates. The first chart shows that exchange rate changes over the following week tend to be in the same direction as suggested by speculative positioning in the previous week. Since February 2024, the ZAR’s relationship with speculative positioning data has changed . As discussed in an earlier post, rand has depreciated despite there being a net long speculative position reported by the US Commodity Futures Trading Commission.

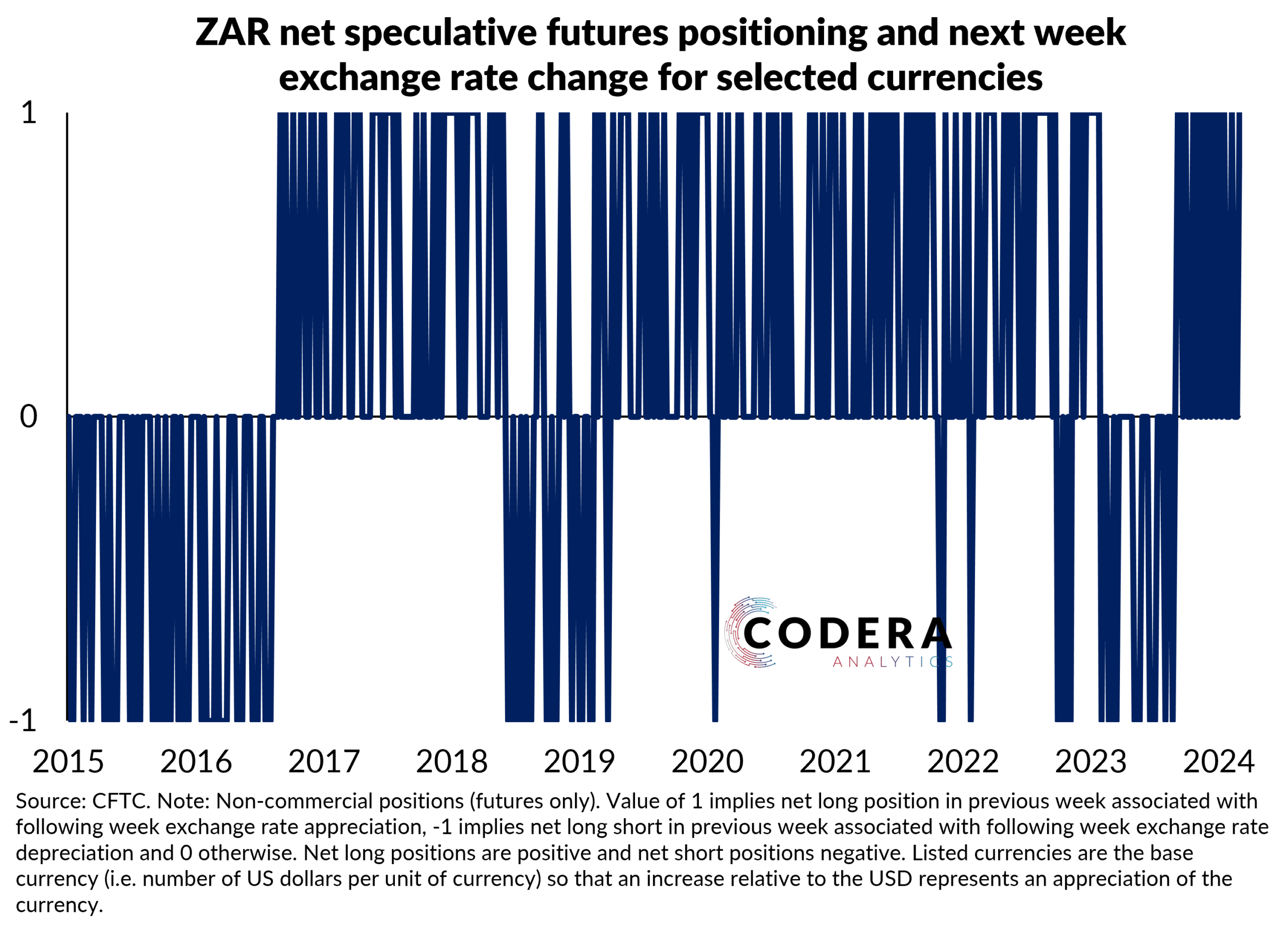

The second chart shows that, in the case of the ZAR, there have been more weeks when a net long position in the ZAR in the previous week was associated with exchange rate appreciation in the following week than weeks when a net short position in the ZAR in the previous week was associated with exchange rate depreciation.

But are speculative positioning data statistically significant predictors of exchange rate movements? If one formally evaluates the predictive content of FX positioning data, it is mainly useful for interpreting historical exchange rate changes, with their use as a predictor of exchange rates being rather limited.