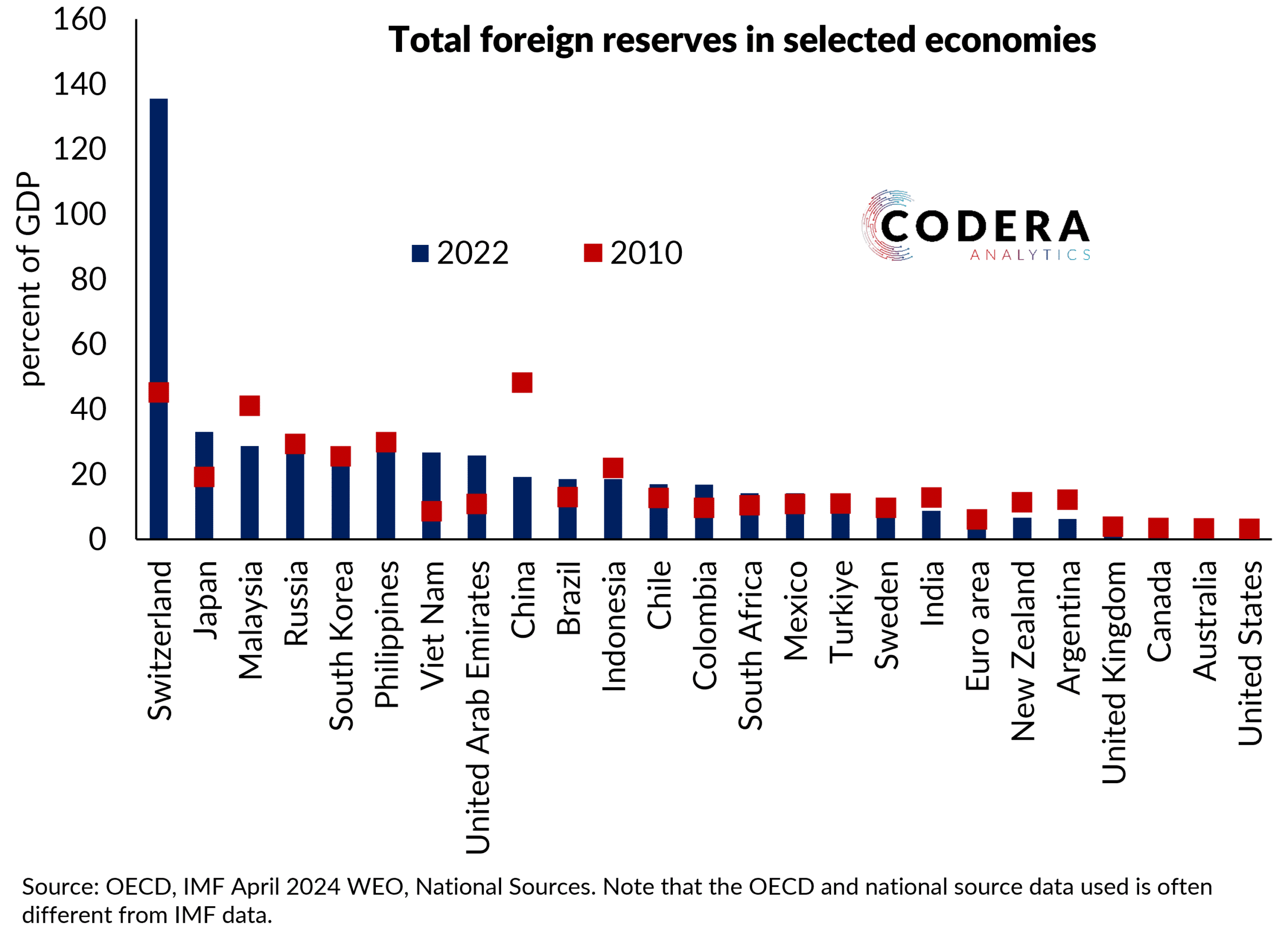

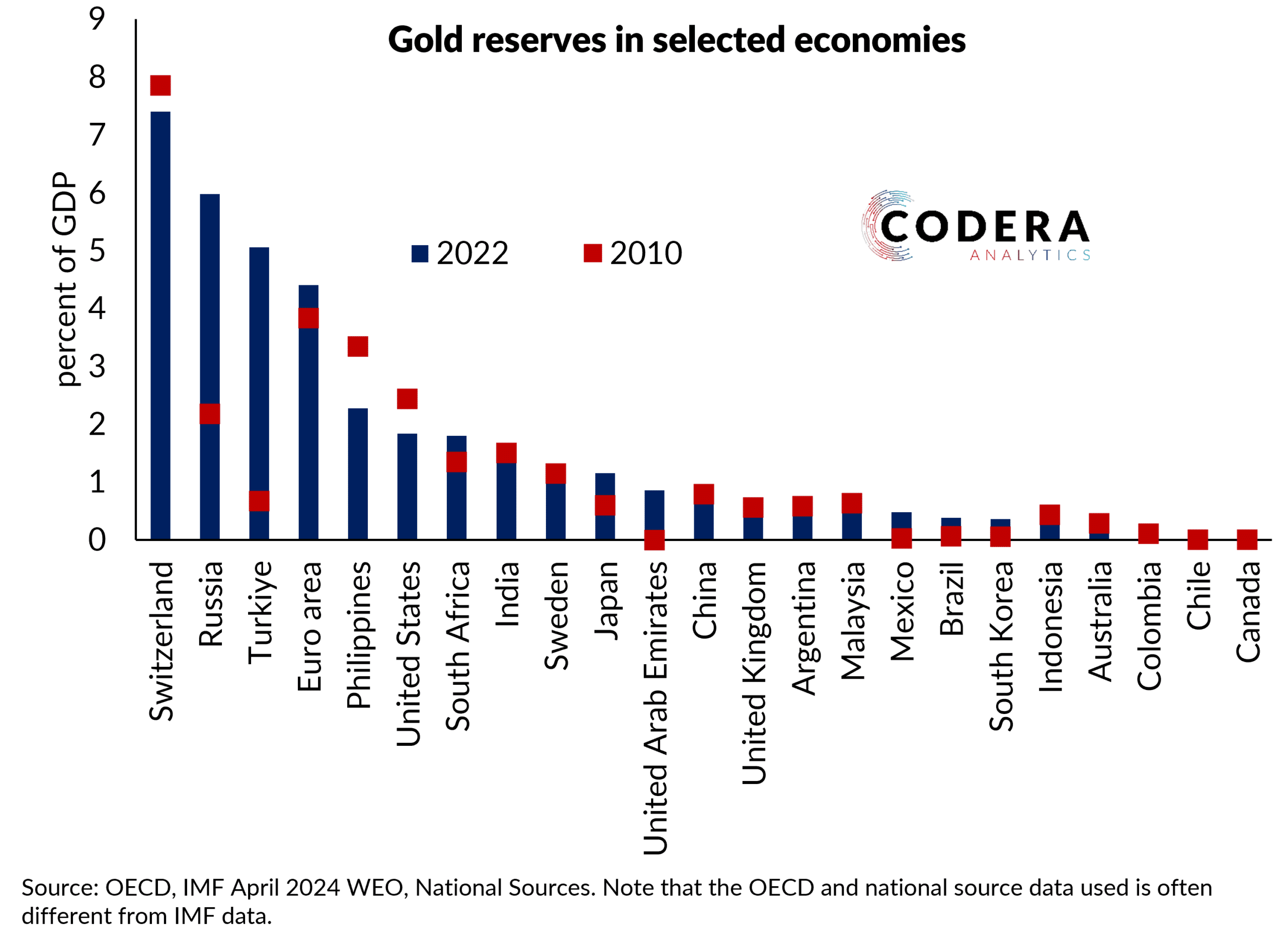

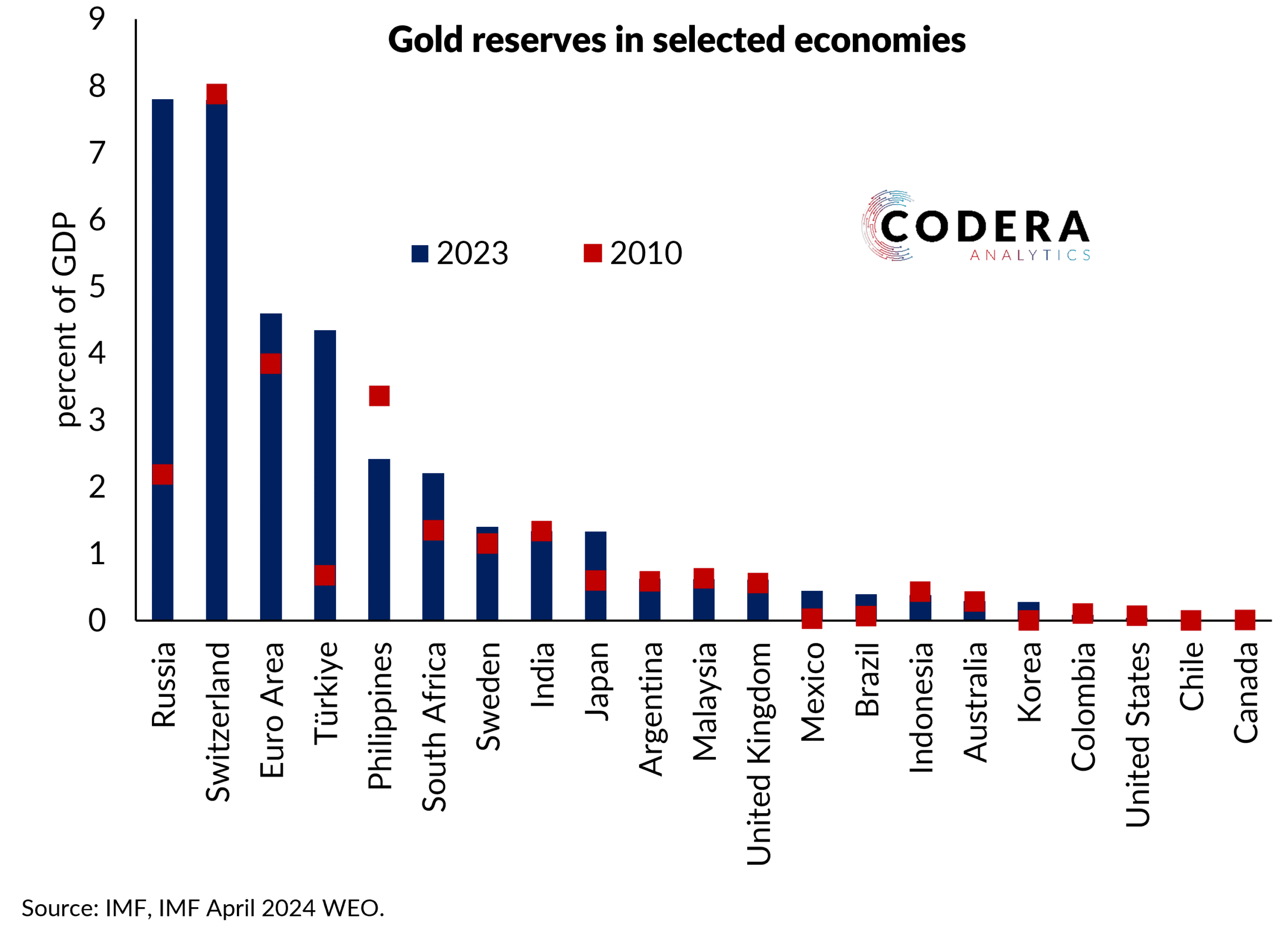

Among major economies, Switzerland stands out for the extent of the increase in its foreign reserves since the global financial crisis. South Africa’s foreign reserves stand at above 16% of GDP, at a comparable relative level to Brazil and India. South Africa also has a relatively high level of gold reserves.

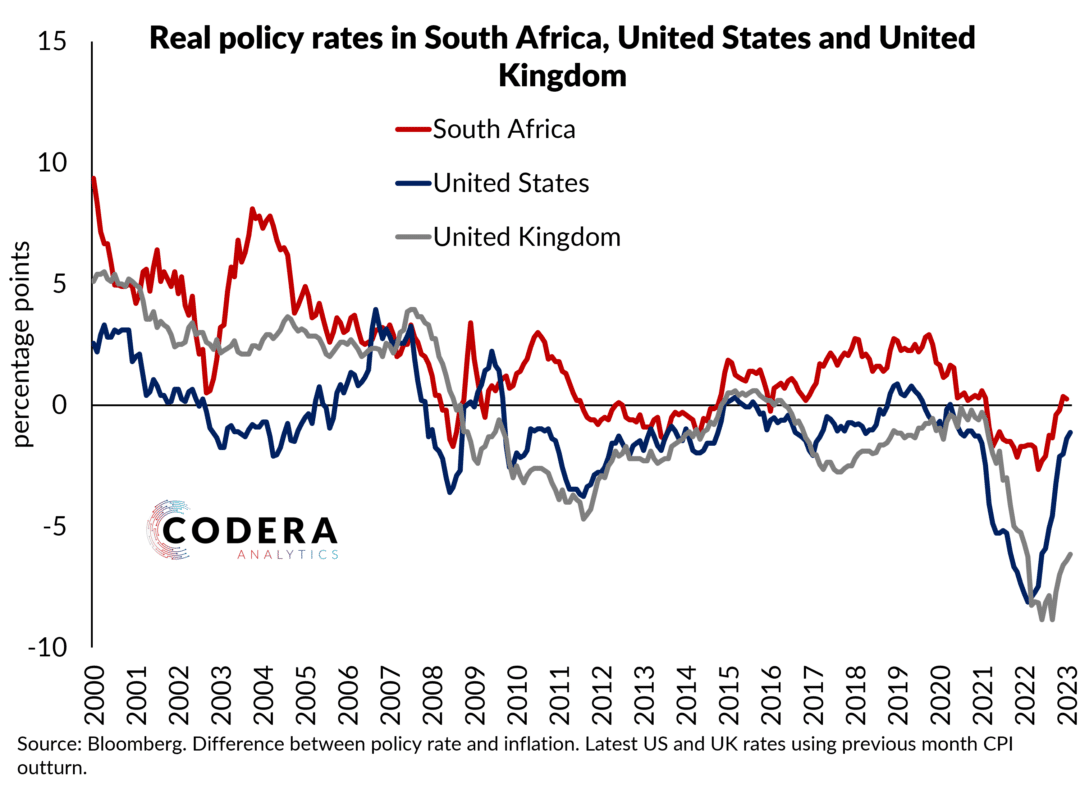

The IMF’s assessment of foreign reserve adequacy across countries finds that South Africa’s reserves meets the IMF’s assessment of an adequate level. In an earlier post, I estimated the implied cost of holding foreign reserves. I estimated that South Africa’s median valuation gain (which will include the impact of currency changes) has been around 1% of GDP against a median carry cost of 0.5% of GDP.

A policy question few seem to ask is whether spending something in the order of 0.5% of GDP per year on reserves as an insurance policy offers value for money or not for SA Inc. Should South Africa accumulate reserves over time as the IMF suggests, or pay off its debt more quickly, given how steep South Africa’s yield curve is? The government has recently decided to monetise unrealised profits from the Reserve Bank’s Foreign Exchange Contingency Reserve Account (GFECRA). As I have argued previously, whether this is a good idea depends on one’s view of what the appropriate foreign reserve strategy for South Africa is.

Footnote

Footnote

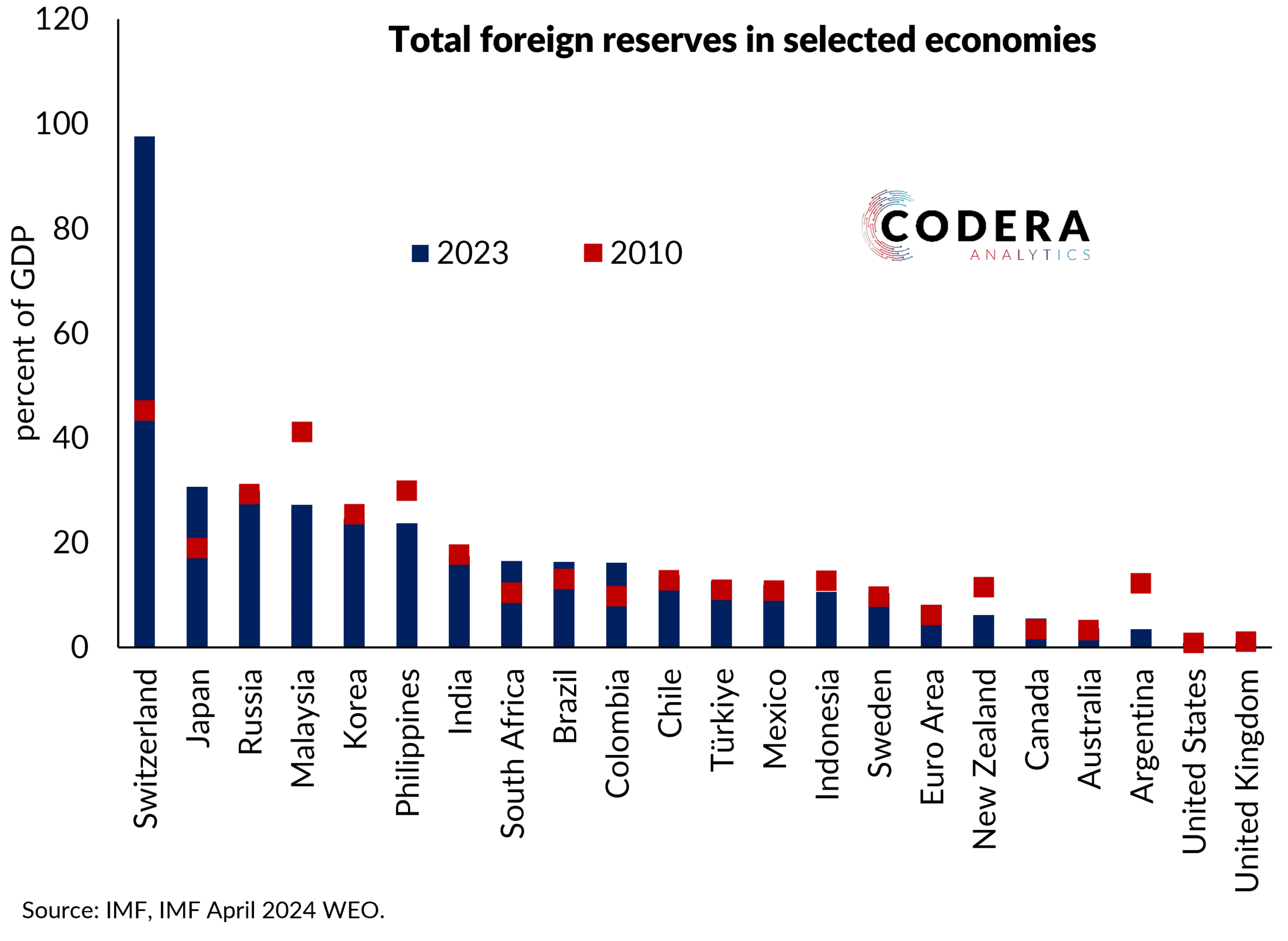

There are important differences between data sources. Below is a comparison for a larger sample of economies based on OECD reserves data and IMF GDP.